We recently advised a Polish medtech company developing an innovative artificial intelligence-powered Software as a Medical Device (SaMD) designed to support early detection of cardiovascular disease based on standard electrocardiogram (ECG) recordings.

The client is developing software that performs automated analysis of resting ECG data and generates additional diagnostic insights for physicians. While the patient experience remains identical to a standard ECG examination, the software applies advanced signal processing and AI-driven analytics to extract significantly more information from the underlying electrical activity of the heart. The current version is intended for use in clinical settings, while a next-generation solution is being developed for home use, enabling remote screening and telemedicine-based monitoring.

Labor law is a key area of the legal system, directly impacting the professional and social situation of millions of employees and employers. Dynamic changes in the labor market, technological progress, and economic conditions necessitate adapting legal regulations to new realities. Recently, we have observed increased legislative activity in this area, not only in Poland but also in the EU. The Labor Code is amended almost annually. This year, 2026 will be no different. This time, however, the amendments will affect a very large portion of society and will address issues such as seniority, salary transparency, recruitment neutrality, and even the gender pay gap. Therefore, for context, it is worth reviewing the new regulations that entered into force at the end of 2025, and then moving on to those that await us this year. At the end of this article, we will also highlight possible legal changes that have been announced for a long time. Their implementation is highly probable and could bring significant changes. Therefore, it is worth being aware of them.

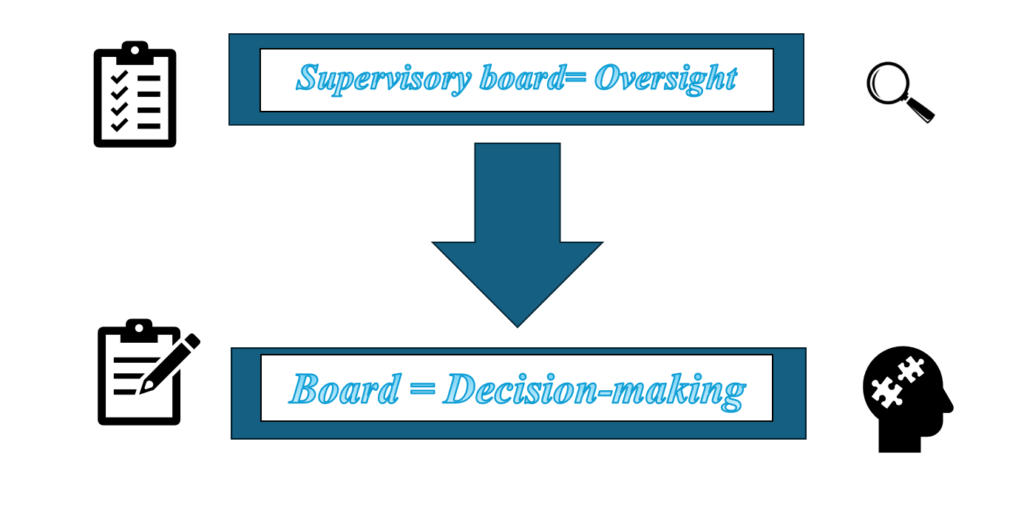

The supervisory board is one of the key bodies of a company, performing the function of constant oversight of the company’s activities in all areas of its operation. Its constitutional position is established as a separate body from the management board, deprived of the authority to manage the company’s affairs, but equipped with control instruments aimed at protecting the interests of the company and its shareholders. This structure is based on a clear separation of decision-making and supervisory functions, which, at least at the normative level, is intended to ensure the proper functioning of corporate governance mechanisms. However, business practice and extensive case law demonstrate that the boundaries between the powers of the supervisory board and the management board are not always clear. In particular, disputes focus on the scope of the supervisory board’s interference in the company’s day-to-day operations, the nature and effects of its resolutions, its communication relations with the management board, and the legal consequences of exceeding its authority. These issues most often arise in the context of the civil liability of supervisory board members and the assessment of the legality of their actions under the provisions of the Commercial Companies Code. The purpose of this article is to present selected issues related to the functioning of the supervisory board in companies against the background of court case law. This analysis focuses in particular on the liability of supervisory board members for damages, conflicts of authority with the management board, the risk of violating the law while performing supervisory functions, and formal issues related to the composition and operation of company bodies. This approach allows us to present the supervisory board not only as a formal control body, but also as an entity that actually contributes to shaping the company’s legal situation and bears the consequences of its actions or omissions.

An unauthorized transaction is a financial transaction made without the consent of the account or cardholder, for example, as a result of data theft. In such a situation, the bank is obligated to return the funds unless it can prove the customer’s intentional act or gross negligence.

Currently, there is a noticeable increase in unauthorized transactions. This causes payers and banks to lose nearly a billion złoty annually. The Polish Financial Ombudsman is noticing a growing number of requests for intervention regarding unauthorized payment transactions. In the first half of 2020 alone, it received 416 requests. This is more than in all of 2018, when there were 367. In 2019, there were 612 requests, an increase of almost 60%. It is worth noting that in the first half of 2020, requests regarding unauthorized transactions accounted for 80% of all requests related to violations of the Payment Services Act.

Modern medical devices used in plastic surgery and aesthetic medicine now operate within an exceptionally complex regulatory environment. The issue no longer concerns only product safety itself, but above all the boundary between permissible information, advertising, and the legal architecture of digital communication platforms used by manufacturers in the life sciences sector.