The beneficial owner clause is used in the so-called withholding tax. Withholding tax is a flat-rate income tax collected by a tax remitter based in the country where the income was generated. It is collected before the income (e.g. from dividends) is paid to an entity that does not have its registered office in Poland. Sometimes (e.g. under Article 22(4) of the CIT Act) the tax remitter is entitled to an exemption. This is usually the case if the entity to which the payment will be made is based in the EU, the European Economic Area or a country that is a party to a double tax treaty with Poland. In such a case, it is necessary to determine whether the entity to which the payment is to be transferred is the beneficial owner of the payment and, if so, where it is subject to taxation.

During the 38th NATO Summit in The Hague in June 2025, the importance, strength, and durability of the North Atlantic Alliance were confirmed in a short declaration consisting of only five short points, including the unwavering validity of Article 5 of the North Atlantic Treaty (Washington Treaty) of April 4, 1949.

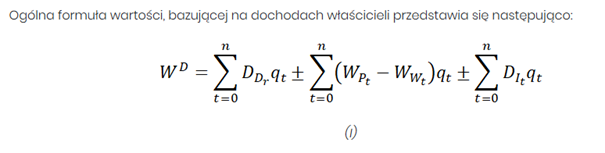

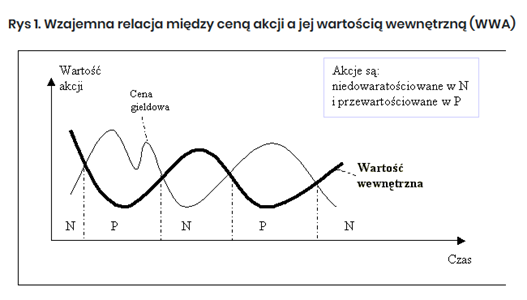

In this article attention will be paid to the valuation of the company’s shares:

When is a stock valued at the day’s price?

When is a stock valued at its mid-year average price?

The topic will be analyzed from an economic perspective. Additionally, these aspects will include situations in which one of the previously mentioned valuations is used and why it works well in those situations.

Stock Valuation

Stock valuation is a key process for investors, allowing them to assess investment risk and helping them decide whether to buy or sell a stock. There are several stock valuation methods that provide information about whether a company is undervalued or overvalued.

A family foundation is a legal structure that builds an organizational structure aimed at securing family assets. It acts as a kind of treasure trove for the founder, protecting his family and business from accidents. Such foundations are popular in other countries such as Austria, Liechtenstein, Germany and Switzerland. A family foundation operates on the basis of a statute (and any regulations), with the founder having a great deal of freedom in determining the principles of its operation. Thanks to the flexibility in shaping the foundation structure and favorable taxation rules (the effective rate is about 13%), it is a tool ideally suited to the expectations of entrepreneurs who have long advocated for the introduction of such a solution in the Polish legal system. The interested party (the founder) is able to draw up a will as well as to establish a family foundation during their lifetime, which will manage their assets.

The name “yellow trade unions” itself may have at least two sources. According to one, it refers to the “yellow dog clauses”, which in the past referred to provisions of employment contracts prohibiting joining trade unions. Another possible etymology was the workers’ organizations operating in France at the beginning of the 20th century, which, in order to distinguish themselves from the communist “red” organizations, called themselves “yellow”.