Types of white-collar crime under Polish law based on recent provisions

Publication date: May 26, 2025

According to Article 7 § 2 of the Polish Penal Code, a crime is “a prohibited act punishable by imprisonment for a period of not less than 3 years or by a more severe penalty.”

Vat crime will be an offence described in:

Art. 277a. [Forgery of invoices with an amount due exceeding PLN 10 million]

§ 1. Whoever commits the offence specified in Article 270a § 1 or Article 271a § 1 with respect to an invoice or invoices containing a total amount due, the value or total value of which is greater than ten times the amount defining the property of great value, shall be subject to the penalty of deprivation of liberty for a term of between 5 and 25 years.

This qualification is possible in the case of taking action under Article 270a § 1 of the so-called material forgery of invoices or Article 271a § 1 of the so-called intellectual forgery of invoices. The first of the above-mentioned offences means forging invoices within the scope relevant to determining tax liabilities. The second prohibited act is directed at the intraneus, being the issuer of the invoice, who falsifies circumstances relevant to determining the tax liability. “These invoices do not reflect the transactions actually carried out. They were issued in order to create input tax for their recipients.”[1] As can be seen, both prohibited acts are offences, only the occurrence of the qualified type under Article 277a, i.e. forgery resulting in an increase in the liability by more than PLN 10,000,000[2]. The implementation of the features of the prohibited act under Article 277a is possible only when the value (or total value) of the total amount of the liability is greater than ten times the amount defining the property of great value. According to art. 115 § 6, property of great value is property whose value at the time of committing the prohibited act exceeds PLN 1,000,000. Consequently, the total amount of receivables under art. 277a must exceed PLN 10,000,000. This crime is exclusively intentional.

Extraordinary leniency is possible

Art. 277c. [Extraordinary mitigation of punishment or waiver of punishment against the perpetrator of the offence of invoice forgery]

§ 1. At the request of the prosecutor, the court shall apply extraordinary mitigation of punishment to the perpetrator of the offence specified in Article 270a § 1 or 2 or Article 271a § 1 or 2, who notified the body responsible for prosecuting offences about it and disclosed all the essential circumstances of the offence, as well as indicated the acts related to the offence committed by him and their perpetrators before that body learned about them.

§ 2. At the request of the prosecutor, the court may refrain from imposing a penalty on the perpetrator of the offence specified in Article 270a § 1, 2 or 3, Article 271a § 1, 2 or 3 or Article 277a § 2, who, in addition to fulfilling the conditions specified in § 1, returned the financial benefit obtained from committing this offence in whole or in a significant part.

§ 3. The court may apply extraordinary mitigation of punishment to the perpetrator of the offence specified in Article 277a § 1, who, in addition to meeting the conditions specified in § 1, returned the financial benefit obtained from committing this offence in whole or in a significant part.

| Legal provision | Name of the prohibited act | Features of a prohibited act | Sanction |

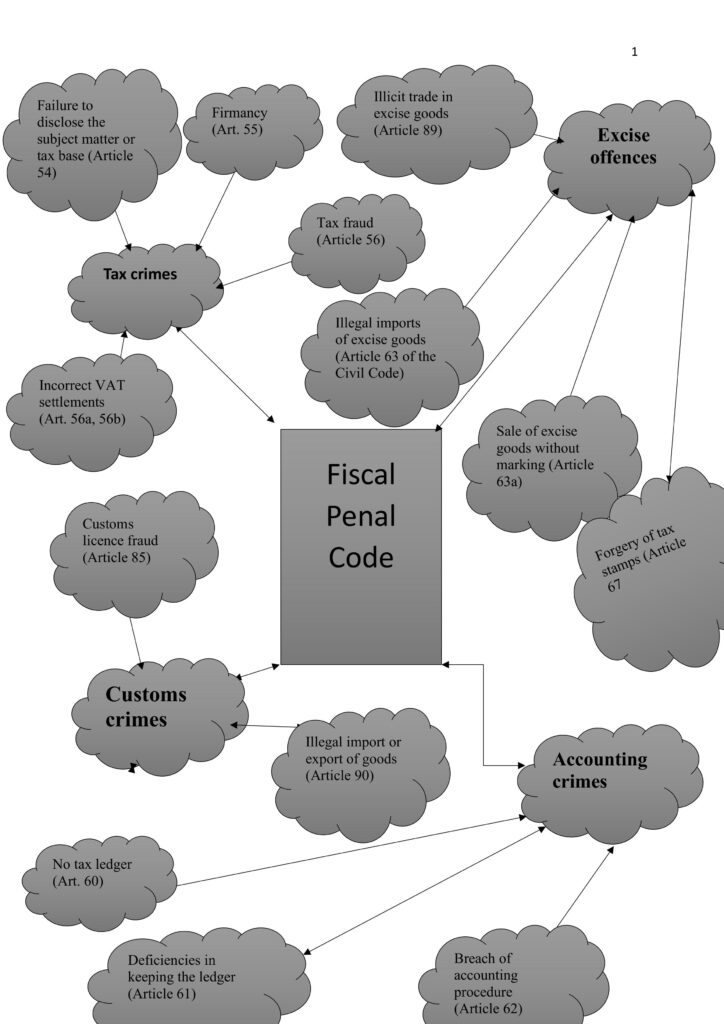

| Article 54 | Failure to disclose the subject or basis of taxation | failure to disclose the subject or basis of taxation.failure to submit a declarationfailure to report income from illegal activities for tax purposes | a fine of up to 720 daily rates deprivation of liberty both penalties together |

| Article 55 | Commercial crime | concealment of business activitiesindividual character | a fine of up to 720 daily rates 3 years imprisonment Both penalties combined |

| Article 56 | Tax fraud | Individual nature and committed by the taxpayerproviding false information or concealing the truth in a declaration or statementfailure to comply with the obligation to notify the above-mentioned bodies or the payer about any change in the data covered by such a declaration or statement. | Fine up to 720 daily rates Deprivation of liberty Both penalties together |

| Article 56a | Failure to submit information on vehicles to the relevant tax authority | does not submit the above information on vehicles to the relevant tax authority or submits it after the deadline or provides data that is inconsistent with the actual state of affairs. However, in order to meet the characteristics of the act under Article 56a § 1 of the Fiscal Penal Code, it is necessary for the taxpayer to deduct tax in breach of the provisions of the Goods and Services Tax through one of the above-mentioned conducts. | Fine up to 720 daily rates |

| Article 56b | Violation of the regulations on registration of entities in the field of excise tax | failure to submit an application for entry into the register of intermediary tobacco entities,providing data in the application for entry into this register that is inconsistent with the actual state of affairs,failure to notify about discontinuation of business as a tobacco intermediary,submitting a notification of discontinuation of business as a tobacco intermediary after the deadline,providing data in this notification that is inconsistent with the actual state of affairs,failure to notify about a change in the data contained in the application for entry into the register of tobacco intermediaries,failure to notify about a change in the data contained in the application to change the entry in the register of intermediary tobacco entities,submitting the above-mentioned applications after the deadline,providing data in the above-mentioned applications that is inconsistent with the actual state of affairs. | A fine of 720 daily rates |

| Art. 56c | Violation of the provisions on submitting declarations on the preparation of local transfer pricing documentation | Neglect of the obligation to prepare local and attach group transfer pricing documentation | |

| Art. 56d | Providing false information or concealing the truth in selected statements related to income taxes | providing false information or concealing the truth when submitting statements or information | A fine of 720 daily rates |

| Article 56e | Failure to submit the required declaration by a shareholder or stockholder of a taxpayer taxed with a lump sum on corporate income, submitting it after the deadline or providing false information therein | failure to submit to the taxpayer the declaration referred to in Article 28s paragraph 1 of the CIT Act,submitting such a declaration after the deadline orproviding data in this declaration that is inconsistent with the actual state of affairs. | A fine of 720 daily rates |

| Art. 56f | Failure to submit the required information on equalisation taxation, submitting it in a manner inconsistent with the requirements or after the deadline, or providing false information therein | Failure to submit the required information on equalisation taxation, submitting it in a manner inconsistent with the requirements or after the deadline, or providing false information therein | A fine of 720 daily rates |

| Article 57 | Persistent non-payment of tax | Repeatedly and negligently paying tax despite obligation. | a fine for a fiscal offence |

| Article 57a | Violation by the bailiff of the obligation to transfer enforcement fees to the tax office | The bailiff does not transfer the enforcement fees to the account of the relevant tax office or transfers them in the wrong amount | A fine of 720 daily rates or imprisonment, or both. |

| Article 57b | Violation by the bailiff of the obligation to submit monthly information on enforcement fees received | The bailiff does not pay the amount due to the appropriate head of the tax office in accordance with the act on judicial bailiffsHe pays the amount due after the deadline | a fine of up to 720 daily rates |

| Art. 57c | Making payments without using the split payment mechanism | Failure to make a payment using the split payment mechanism | a fine of up to 720 daily rates |

| Article 60 | No bookkeeping | the act of not carrying out bookkeeping | a fine of up to 240 daily rates |

| Article 61 | Bookkeeping deficiencies | an act of dishonest bookkeeping | a fine of up to 240 daily rates |

| Art. 61a | Violation of the obligation to send the book to the relevant tax authority | an act of failing to send the book to the appropriate tax authority or sending an unreliable one | a fine of up to 240 daily rates |

| Article 62 | Violation of accounting procedure | does not issue an invoice or bill, issues them incorrectly or refuses to issue themissues an invoice or bill in an unreliable manner or uses such a documentissues an invoice or bill in an unreliable manner or uses such a document, and the tax amount resulting from the invoice or the sum of the tax amounts resulting from the invoices is of low value | A fine of 720 daily rates or imprisonment, or both. |

| Article 63 | Illegal import of excise goods | issues excise goods for which the excise duty suspension procedure has been completed, without previously marking them with excise duty stampsimports excise goods into the country without first marking them with excise stampsproducing excise goods outside the tax warehouseremoves from a tax warehouse on the basis of a permit to remove excise goods from another person’s tax warehouse as a taxpayer outside the excise duty suspension procedureincorrect determination of excise stamps | A fine of 720 daily rates or imprisonment, or both. |

| Art. 63a | Sale of excise goods without marking them with excise stamps | Sale of excise goods without prior correct marking with appropriate excise stamps | A fine of 720 daily rates or imprisonment, or both. |

| Article 64 | Illegal export of excise goods | removal of products from the tax warehouse premises outside the excise duty suspension procedure | A fine of 720 daily rates |

| Article 65 | Excise handling of stolen goods | an act of acquiring, storing, transporting, sending or transferring excise goodshelping to dispose of them, or receiving them or helping to conceal them | A fine of 720 daily rates or imprisonment, or both. |

| Article 66 | Incorrect excise product marking | incorrect marking of excise goods with excise stampsmarking them with incorrect excise stamps | shall be subject to a fine of up to 720 daily rates |

| Article 67 | Forgery of excise stamp | Forgery of excise stamps | a fine of up to 720 daily rates |

| Article 67a | Possession of false excise stamps or authorisation to receive excise stamps | the act of possessing, storing, transporting, sending or transferring counterfeit or altered excise stamps or authorisation to receive excise stamps is penalised. | a fine of up to 720 daily rates or imprisonment, or both. |

| Article 68 | Failure to comply with the obligation to mark an excise product | an act of failing to fulfil the obligation to prepare a list and submit it for confirmation to the competent authorityan act consisting in failure to fulfil the obligation to mark excise goods with legalisation excise stamps | a fine of up to 720 daily rates |

| Article 69 | Illegality of commercial activities | acts against obligations related to the production, import and trade of excise goods and their marking with excise stamps were typified. | 720 daily rates 360 daily rates 240 daily rates |

| Article 69a | Carrying out activities outside a tax warehouse | acts violating the provisions on the excise duty suspension procedure | a fine of up to 720 daily rates or imprisonment, or both |

| Article 69b | Making an intra-Community delivery or intra-Community acquisition of excise goods in breach of the regulations | the prohibited act of making an intra-Community supplyintra-Community import of excise goods in violation of the provisions of the Act | a fine of up to 720 daily rates or imprisonment, or both a fine for a fiscal offence |

| Art. 69c | Movement of excise goods without the required documentation | Movement of excise goods without: without an e-SAD document or a document replacing the e-SAD or without an e-AD printout with an assigned reference number or another commercial document in which the reference number assigned to the e-AD in the system is included or a document replacing the e-ADbased on these documents containing data inconsistent with the actual state | a fine of up to 720 daily rates or imprisonment, or both |

| Article 70 | Disposal of an excise stamp to an unauthorized person | acts concerning illegal trade in excise stamps. The punishability of such conduct results from the regulation of trade in excise stampsa prohibited act consisting in selling or otherwise transferring excise stamps to an unauthorized person | A fine of up to 720 daily rates or imprisonment, or both. |

| Article 71 | Incorrect transportation of excise stamps | an act of exposing excise stamps to a direct risk of theft, destruction, damage or loss, which is the result of a gross violation of the regulations on the transport or storage of excise stamps. | a fine of up to 480 daily rates |

| Article 72 | Failure to settle excise duty stamps | an act of failing to settle the usage of excise stamps with the competent authority on time, in particular failing to return unused, damaged, destroyed or invalid stamps | Fine of up to 360 daily rates |

| Article 73 | Change of excise product marking | an act consisting in changing the purpose, intended use or failure to comply with another condition on which the act makes the exemption of an excise product from the obligation to mark it with excise stamps dependent | A fine of 720 daily rates. |

| Art. 73a | Improper use of excise goods | changing the purpose of the excise product in its use, resulting in the risk of excise duty reduction | a fine of up to 720 daily rates or imprisonment for up to 2 years, or both. |

| Article 75 | No daily excise report | an act consisting in failing to fulfil the obligation to obtain from an entity established outside the territory of the country a settlement of the excise tax stamps transferred to it. | Fine of up to 180 daily rates |

| Article 75a | Failure to carry out measurements in accordance with the principles of the Act on the tax on the extraction of certain minerals | an act consisting in the taxpayer failing to pay tax on the extraction of certain minerals contrary to the obligation to measure the content of copper and silver in copper ore or concentrate or making measurements in violation of the principles specified in art. 15 sec. 1 points 2 and 3 , sec. 2 points 2 and 3 and sec. 3 of the Upwnk Actexposure of the tax on the extraction of certain minerals to depletion. | a fine of up to 720 daily rates or imprisonment for up to 2 years, or both. |

| Art. 75b | Failure to keep records in accordance with the principles of the Act on the tax on the extraction of certain minerals | Acts of failing to keep accounting records or keeping them in an unreliable or defective manner | a fine of up to 360 daily rates. Fine of up to 360 daily rates |

| Art. 75c | Conducting copper and silver mining activities without official verification | an act of conducting business in the field of copper, silver, natural gas or crude oil extraction without conducting official verification | a fine of up to 720 daily rates |

| Article 76 | Unjustified tax refund | providing data inconsistent with the actual state of affairs or concealing the actual state of affairs. | a fine of up to 720 daily rates or imprisonment, or both. |

| Article 76a | Providing false information or concealing the actual state of affairs | refers to the reimbursement of expenses made pursuant to the Act of 29 August 2005 on the reimbursement to individuals of certain expenses related to housing construction | a fine of up to 720 daily rates or imprisonment for up to 5 years, or both. |

| Art. 76b | Providing false information or concealing the actual state of affairs | exposure to undue reimbursement of expenses, thus creating a risk of undue reimbursement of expenses | a fine of up to 720 daily rates or imprisonment for up to 5 years, or both. |

| Article 77 | Failure to pay collected tax | failure to pay the tax withheld in relation to the taxpayer’s failure to pay the tax | a fine of up to 720 daily rates or imprisonment for up to 3 years, or both. |

| Article 78 | Violation of tax procedure | failure to collect tax and collection of tax in an amount lower than that due. | a fine of up to 720 daily rates or imprisonment for up to 2 years, or both. |

| Article 79 | No tax calculator or tax collector | failure to fulfil certain obligations incumbent on these entities, not of a fiscal nature. | fine for a fiscal offence. |

| Article 80 | Violation of tax information filing requirement | acts related to neglecting the obligation to submit tax information or certain other information and submitting such false information. | Fine from 120 to 240 daily rates |

| Article 80a | Irregularities in the summary information | Deliberately introducing irregularities into the summary information | a fine of up to 240 daily rates. |

| Art. 80b | Failure to fulfil the obligation to submit the financial statement or audit report to the relevant tax authority on time | failure to submit a financial report or an audit report to the Head of the National Tax Administrationsubmitting them after the deadline | a fine for a fiscal offence |

| Art. 80c | Failure to comply with obligations arising from the provisions on the exchange of tax information with other countries | failure to fulfil the obligations under Article 27 section 1 of the Public Procurement Lawpoint 4 penalises failure to fulfil the obligations to remove irregularities indicated in a timely manner as a result of an inspection of the reporting financial institution’s performance of its obligations in the scope of applying due diligence procedures and reporting procedures, which the Head of the National Tax Administration is authorised to conduct | fine for a fiscal offence. |

| Art. 80ca | Failure to fulfil the obligation to provide tax information at the request of the minister or the Head of the National Tax Administration | penalizes conduct consisting in submitting false information for the purposes of information about entities included in a group of entities | a fine of up to 240 daily rates. Or a fine for a fiscal offence. |

| Art. 80cb | Failure to fulfil the obligations incumbent on the reporting platform operator | 1) applying due diligence procedures, including collecting required documentation, 2) providing the Head of the National Revenue Administration with information about sellers, 3) one-time registration in the Republic of Poland in the absence of registration in another selected Member State, 4) failure to remove irregularities indicated as a result of the inspection within the deadline referred to in Art. 75zb sec. 4 of this Act shall be subject to a fine of up to 180 daily rates. | a fine for a fiscal offence |

| Art. 80d | Submitting false information about entities included in a group of entities | conduct consisting in submitting false information for the purposes of information about entities included in a group of entities | a fine of up to 240 daily rates |

| Art. 80e | Breach of the obligation to submit information on transfer prices | the act of failing to submit information on transfer prices to the relevant tax authorityproviding data that is inconsistent with the local transfer pricing documentation or the actual state of affairs | a fine of up to 720 daily rates |

| Art. 80f | Breach of obligations related to the provision of information on tax schemes | an act of failing to provide the competent authority with information on the tax scheme or data relating to entities to which the standardised tax scheme was made availablesubmitting these – respectively – information and data after the deadline. | a fine for a fiscal offence or ban on conducting specific business activities |

| Art. 80g | Breach of obligations related to submitting notifications about the management of a warehouse used in the call-off stock procedure | the act of failing to submit a notification of the operation of a warehouse used in a call-off stock proceduresubmitting such a notification after the deadline and providing data inconsistent with the actual state of affairsan act consisting in failure to submit a notification of a change in the data contained in the notification, submitting it after the deadlineproviding data that is inconsistent with the actual state of affairs | a fine for a fiscal offence |

| Art. 80h | Failure to submit a timely notification of the data of the component unit submitting information on equalisation taxation | Failure to submit a timely notification of the data of the component unit submitting information on equalisation taxation | a fine of up to 180 daily rates |

| Art. 80i. | A taxpayer who, when submitting a prior notification to a tax authority, provides false information or conceals the truth or fails to fulfil the obligation to notify about a change in the data covered by the notification | A taxpayer who, when submitting a prior notification to a tax authority, provides false information or conceals the truth or fails to fulfil the obligation to notify about a change in the data covered by the notification | a fine of up to 240 daily rates or a fine for a fiscal offence |

| Article 81 | Failure to comply with the obligation to report or update identification | failure to submit an identification notification or update the data covered by it on time, providing data that is inconsistent with the actual state or incomplete, submitting a notification more than once and failure to provide a tax identification number or providing an incorrect number | a fine for a fiscal offence |

| Article 82 | Violation of the provisions on subsidies and subventions | exposing public finances to depletion through undue payment, collection or misuse of subsidies or grants is penalised | a fine of up to 720 daily rates or imprisonment for up to one year, or both |

| Article 83 | Obstructing fiscal or tax audits | acts consisting in preventing or hindering the performance of an official activity by a person authorized to carry out verification activities, tax control, customs and fiscal control, audit, audit activities and verification acquisition. | ban on conducting specific business activities |

| Article 84 | Lack of supervision | failure to fulfil supervisory obligations and allowing the commission of an offence under Chapter 6 of the Penal Code | a fine for a fiscal offence |

| Article 85 | Customs permit fraud | using a permit or other similar document concerning the conditions of foreign trade in goods or services, obtained in the manner specified in Article 85 § 1 of the Penal Code | ban on conducting specific business activities |

| Article 86 | Customs smuggling | the existence of a customs obligation to present or declare the goods to the customs authority and the existence of a customs duty that may be reduced by failure to comply with this obligation | Prohibition conducting specific business activities |

| Article 87 | Customs fraud | the existence of an obligation to present the goods for customs control and the existence of a customs duty that may be reduced by misleading the authority competent to carry out customs control. | ban on conducting specific business activities |

| Article 88 | Violation of the temporary admission procedure | violation of the conditions of the temporary admission procedure | ban on conducting specific business activities |

| Article 89 | Change of purpose of goods | conduct consisting in changing the purpose, intended use or failure to comply with another condition on which the exemption of goods in whole or in part from customs duties, in particular customs duties, or the application of a zero, reduced or preferential customs duty rate is dependent | ban on conducting specific business activities |

| Article 90 | Removal of goods from customs supervision | conduct consisting in removing goods or means of transport from customs supervision. Removing goods from customs supervision gives rise to a customs debt. | ban on conducting specific business activities |

| Article 91 | Customs handling stolen goods | the existence of a customs obligation to present or declare the goods to the customs authority and the existence of a customs duty that may be reduced by failure to comply with this obligation | ban on conducting specific business activities |

| Article 92 | Unjustified refund of customs duties | misleading the competent authority by providing data inconsistent with the actual state of affairs or concealing the actual state of affairs | ban on conducting specific business activities |

| Article 93 | Violation of customs regulations | violation of customs law provisions regarding the conditions of operation of a free customs zone or customs warehouse and the operation of a temporary storage facility. | ban on conducting specific business activities |

| Article 94 | Obstructing customs supervision | It consists in failing to provide – contrary to one’s obligation – oral or written explanations that are relevant to customs control or failing to provide – contrary to one’s obligation – required documents concerning foreign trade in goods or services. | a fine of up to 720 daily rates |

| Article 95 | No customs documents | No customs documents | Fine of up to 180 daily rates |

| Article 96 | No supervision | consists in failing to fulfil the obligation to supervise compliance with the rules applicable in the activities of a given entrepreneur or other organisational unit. This act may only be committed through omission. | a fine for a fiscal offence |

| Article 97 | Foreign exchange permit fraud | obtaining it in such a way that if it were not for the perpetrator’s behavior, the permit would not have been issued | a fine of up to 720 daily rates or imprisonment for up to 2 years, or both |

| Article 100 | Breach of Duty by Resident | A resident who exports, sends or transfers domestic or foreign means of payment to third countries without the required authorisation | a fine of up to 720 daily rates |

| Article 101 | Transfer of funds without the intermediation of a bank | an act consisting in the sale in the country of debt securities with a maturity of less than one year or receivables or other rights that are exercised through monetary settlements without a foreign exchange permit. | ban on conducting specific business activities |

| Article 102 | Resident violation of restrictions | an act consisting in the performance by a resident of the activities specified in this provision without the required foreign exchange permit or contrary to its terms | ban on conducting specific business activities |

| Article 103 | Illegal trading of foreign exchange values | Article 100 § 1 of the Penal Code by a person who does not have the required permit, who uses a person from whom such a permit is not required or who has it, is penalized | a fine of up to 720 daily rates |

| Article 104 | Evading exchange control | an act consisting in opening or maintaining an account by a resident in a bank or a branch of a bank with its registered office in a third country, without the required foreign exchange permit or contrary to its terms. | ban on conducting specific business activities |

| Art. 106c | Monetary settlements | an act consisting in making monetary settlements in foreign exchange transactions with a foreign country without the required foreign exchange permit or contrary to its terms. | ban on conducting specific business activities |

| Art. 106d | Economic activity | an act consisting in conducting business activities consisting in the purchase and sale of foreign currencies and intermediation in their purchase and sale without entry in the register of currency exchange activities or in violation of the provisions of the Act. | a fine of up to 720 daily rates or imprisonment for up to one year, or both. |

| Art. 106e | Failure to provide explanations and documents | failure to provide oral or written explanations and failure to provide required documents related to the scope of control carried out under the provisions of the Foreign Exchange Law. | a fine for a fiscal offence |

| Art. 106f | Failure to declare cash entering or leaving the EU | an act of failing to report to customs authorities or the Border Guard the import into the country or export abroad of foreign currency or domestic means of payment, as well as providing false information in such a declaration. | a fine for a fiscal offence |

| Art. 106h | Failure to comply with customs control requests for the presentation of cash entering or leaving the EU | failure to submit, contrary to one’s obligation, to the customs authorities or the Border Guard authorities, upon their request, foreign currency or domestic means of payment imported into the country or exported abroad | a fine for a fiscal offence |

| Art. 106j | Bypassing the bank intermediary | making a transfer of money abroad or a settlement in the country related to foreign exchange transactions, contrary to the obligation, without the intermediation of an authorised bank, payment institution, electronic money institution or – in the case of settlements in the country – a payment services office. | a fine of up to 480 daily rates. |

| Art. 106k | Violation of the terms of foreign exchange trading | an act consisting in failure to keep, contrary to the obligation, documents related to the foreign exchange transactions made or the currency exchange activities performed | a fine for a fiscal offence |

| Art. 106l | Failure to comply with the obligation to report data | an act consisting in failing to report to the National Bank of Poland, contrary to the obligation, data on foreign exchange turnover or currency exchange activities performed, to the extent necessary to prepare the balance of payments and the international investment position, or reporting data inconsistent with the factual state. | a fine of up to 120 daily rates |

| Art. 106ł | Allowing a prohibited act to be committed | In order for the features of a prohibited act under this provision to occur, the failure to fulfill obligations must be of an intentional nature, in the form of direct or eventual intent. On the other hand, allowing the prohibited act to be committed may be unintentional conduct. | fine |

| Article 107 | Illegal gambling | organizing and conducting gambling games in violation of the provisions of the Act or the conditions of the license or permit | a fine of up to 720 daily rates or imprisonment for up to 3 years, or both |

| Article 107a | Organizing games without security | arranging or conducting gambling games without the required official verification or without imposing the required official closures | a fine of up to 720 daily rates or imprisonment for up to 2 years, or both |

| Art. 107b | Destruction of evidence of participation in lotteries | destruction of tickets, cards or other evidence of participation in a cash lottery, raffle or raffle bingo game without the required notification to the competent authority. | a fine of up to 720 daily rates |

| Art. 107c | Failure to report damage to gaming equipment | the act of failing to notify the competent authority in due time of the destruction or theft of a gaming machine or device. | a fine |

| Art. 107d | Illegal Possession of a Gaming Machine | possession of a gaming machine contrary to the terms of the licence or without the required official inspection or without imposing the required official closures. | a fine of up to 720 daily rates or imprisonment for up to 3 years, or both. |

| Article 108 | Illegal Gambling Games | conducting or organizing these gambling games illegally (without a permit), as well as by a person who has an appropriate permit but violates its terms. | A fine of 240 daily rates |

| Article 109 | Participating in illegal gambling | Participating in illegal gambling | fines up to 120 daily rates |

| Article 110 | Illegal sale of lottery tickets | engaging in the sale of lottery tickets or other evidence of participation in a game of chance, mutual betting or slot machine game. | a fine of up to 360 daily rates or a penalty of restriction of liberty, or both |

| Art. 110a | Illegal advertising for games or betting | an act of commissioning or conducting, in a manner inconsistent with the Act, advertising or promoting cylindrical games, card games, dice games, mutual betting or slot machine games, placing advertisements for such games or bets or providing information about sponsorship by an entity conducting business in the field of such games or bets | a fine of up to 720 daily rates |

| Art. 110b | Enabling a person under 18 to participate in gambling | Enabling a person under 18 to participate in gambling | fine for fiscal offences |

| Article 111 | Lack of proper supervision | fiscal offence of persons supervising the activities of a given entrepreneur or another organizational unit for allowing the commission of a prohibited act specified in Chapter 9 of the Penal Code. This liability is similar to the liability under Article 84 of the Penal Code | a fine |

[1]Judgment of the Regional Administrative Court in Lublin of 6 November 2024, I SA/Lu 512/24, LEX No. 3818164.

[2]Judgment of the Court of Appeal in Warsaw of 24 February 2022, II AKa 448/21, LEX No. 3333438.