Polish Act on the national cybersecurity certification system

Publication date: August 31, 2025

On August 28, 2025, the Polish Act of June 25, 2025, on the national cybersecurity certification scheme, entered into force, implementing Regulation (EU) 2019/881 of the European Parliament and of the Council of April 17, 2019, on ENISA (the European Union Agency for Cybersecurity) and cybersecurity certification in information and communication technologies and repealing Regulation (EU) No 526/2013 ( Cybersecurity Act ) (OJ L 151, 7.06.2019, p. 15 and OJ L 2025/37, 15.01.2025).

What is CSIRT GOV and what is its legislative environment

The Polish Computer Security Incident Response Team (CSIRT GOV), led by the Head of the Internal Security Agency, serves as the national CSIRT. The CSIRT GOV is responsible for coordinating the response process to computer incidents occurring in the area specified in Article 26, Section 7 of the Act of 5 July 2018 on the National Cybersecurity System.

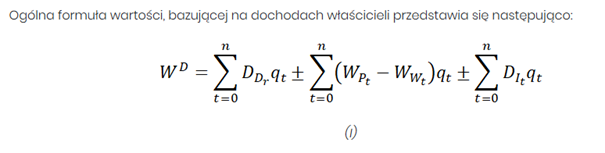

In this article attention will be paid to the valuation of the company’s shares:

When is a stock valued at the day’s price?

When is a stock valued at its mid-year average price?

The topic will be analyzed from an economic perspective. Additionally, these aspects will include situations in which one of the previously mentioned valuations is used and why it works well in those situations.

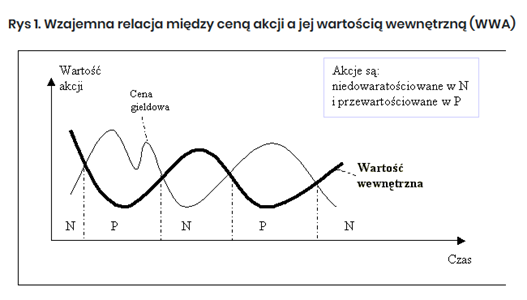

Stock Valuation

Stock valuation is a key process for investors, allowing them to assess investment risk and helping them decide whether to buy or sell a stock. There are several stock valuation methods that provide information about whether a company is undervalued or overvalued.

Dynamic technological advancements have led modern businesses to operate in ways unforeseen decades ago. Computerization, in particular, without which modern business operations are inconceivable, has effectively broadened the horizons of many entrepreneurs, while simultaneously leaving room for abuse by cybercriminals. The protection of data stored on companies’ internal servers has become crucial. It should be noted that despite the efforts of both EU and national authorities, new threats are emerging in the field of personal data protection law, which may lead to violations not only of general provisions on the protection of personal rights but also of many other legal disciplines, such as copyright. The unprecedented mass digitization of artistic works has resulted in the inclusion of records of paintings, photographs, films, music, architectural designs, and many other manifestations of creative activity as data. From this perspective, the phenomenon of data laundering takes on a unique character and carries with it new threats.

The term “carousel fraud” refers to a characteristic scheme in which goods, after passing through a series of related entities, ultimately end up back at the original supplier. This mechanism allows perpetrators to conceal the actual transaction and generate undue tax benefits, most often by fraudulently obtaining VAT refunds or avoiding their payment. A key feature of VAT is its neutrality, so it should not impose an additional burden on taxpayers who do not consume the purchased goods or services but use them for business purposes. However, the structure of this tax makes it particularly vulnerable to abuse. In accordance with the principle of the free movement of goods, the supply of goods between European Union (EU) countries is subject to a 0% VAT rate. VAT carousels involve the use of complex transaction mechanisms embedded in the value added tax structure to avoid paying output tax or to unlawfully obtain a refund. These activities take the form of fictitious economic transactions, which involve the apparent movement of goods between entities located in different Member States. This can be very high, especially with relatively small financial outlays by the fraudsters, as the fraud involves goods that are repeatedly exported and returned to Poland.